What is Wealthsimple? What is a roboadvisor? What is an ETF? Why Mutual Funds are a bad investment option? How can I setup an account? These questions and many more are explained in this video:

What is Wealthsimple?

Wealthsimple is a roboadvisor. Their slogan is “investing on auto pilot” and that boils down to putting your money into the stock market without big fees or complexity.

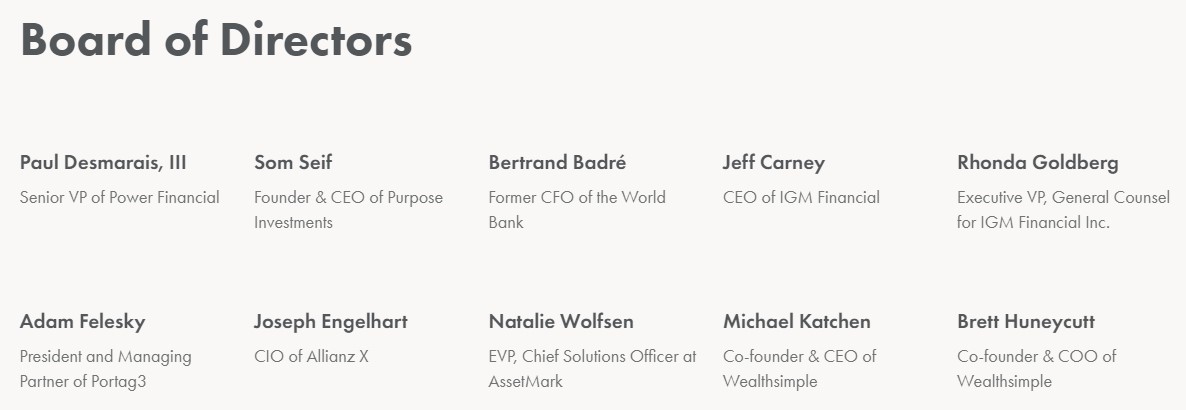

Who Runs Wealthsimple?

Their board of directors include some very big names in the investment world.

Wealthsimple vs Mutual Funds

Most people understand mutual funds in which a guy (…yes a person usually with a small team of researches) takes informed guesses as to which stocks are going up and which ones are going down and then trades those stocks accordingly. This is called active investing and there are two BIG problems with it:

- The profits active investors make are always LESS than what the stock market does on average.

- If you just bought a small number of shares in each of the companies that make up the stock market and held them, you would make more money than if you bought and sold shares in those companies.

- Mutual funds charge about 2.25% of your investment

- that last part of the sentence is key. Mutual funds companies don’t take 2.25% of you profits, they take 2.25% of every dollar you invest regardless of if they made or lost you money

Wealthsimple invests primarily in something called ETF’s. ETF is an acronym for “Exchange Traded Fund” and they are simple an exact copy of the market.

For example, you have probably heard of the S&P500 or the TSX300. The S&P500 is the Standard & Poors stock market top 500 companies. The TSX 300 is the Toronto Stock Exchange 300 top companies. The people that run those stock exchanges decide which companies are included in the their 500 or 300 or… whatever index they decide to build. So why not just buy a shares in each of the companies in the S&P500 or the TSX300 or the FTSE100 (London England) or the Nikkei 225 (Japan)? That is what an ETF is; buying a share of each company in an index.

ETF’s diversify your risk. When Hewlett Packard and Bank of America got into trouble the Dow Jones Stock Exchange continued to allow them trade on their platform, but they were removed from the “Dow Jones Index” . This meant that all EFT’s matching the Dow Jones immediately sold HP and Bank of America and bought the two companies the Dow Jones replaced them with, Nike and Visa. They did not have to do any costly research, they just did it. For that service ETF’s charge an average of .31% which is waaaaay less than 2.25% your mutual fund hustler sells.

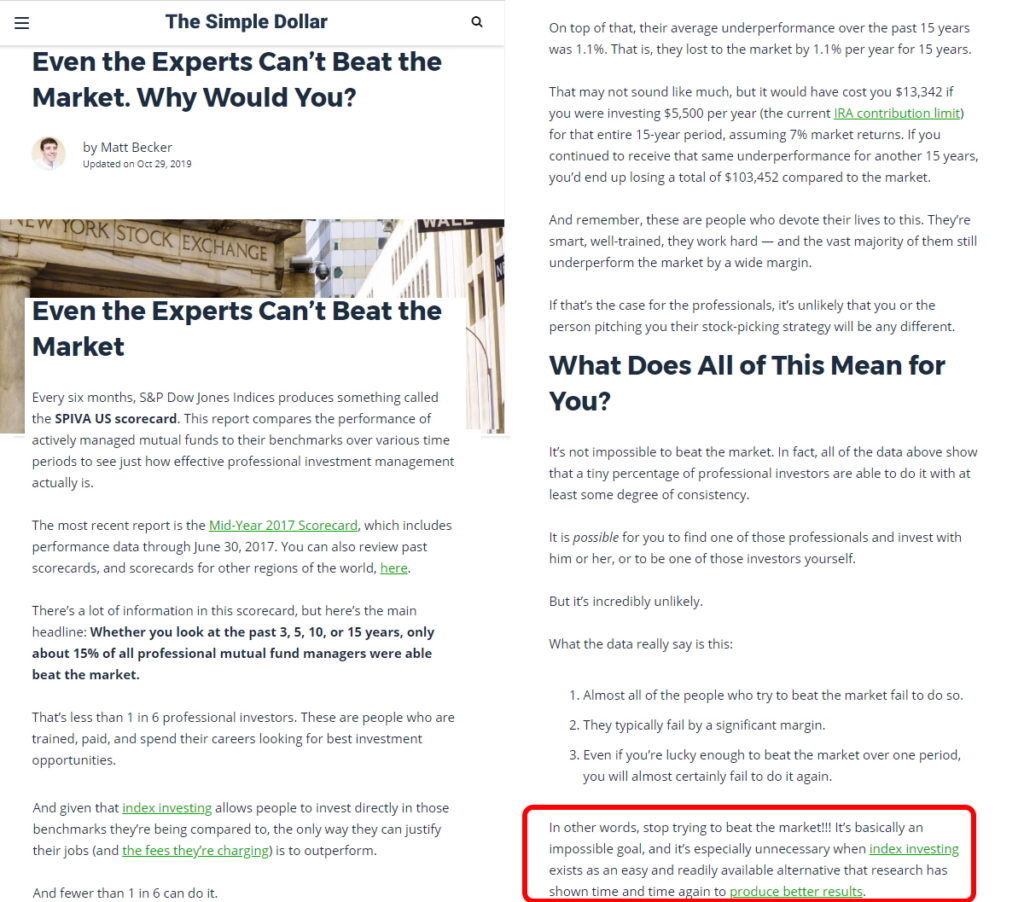

Do you think you or your investment advisor can do better than the average of the market? Well, they can’t. It has been shown in dozens of studies that buying individual stocks is a fools game.

Wealthsimple Is More than ETF’s

Wealthsimple Is More than ETF’s

If Wealthsimple just bought a single ETF, you should not use them because you can just buy the ETF yourself. Wealthsimple invests in many ETF’s to spread your risk.

They also buy government and corporate bonds (debt!). So when Audi or the US Government or Microsoft or Costco want to borrow money they put out what is known as “debentures”. These are just dept notices and big companies buy portions of that dept. For example, in May 2020 Apple borrowed $8 billion dollars and companies like Wealthsimple bought tiny portions of that debt which is paying .75% interest. I think you would agree that it highly unlikely that Apple will not be able to pay that money back so for Wealthsimple this is a way to reduce their risk and therefore your risk.

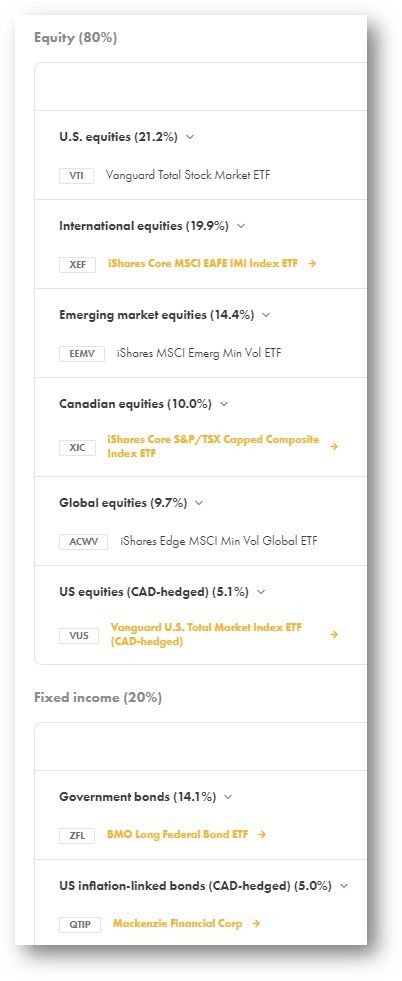

If you click on the image to the right you will see what Wealthsimple has me invested in.

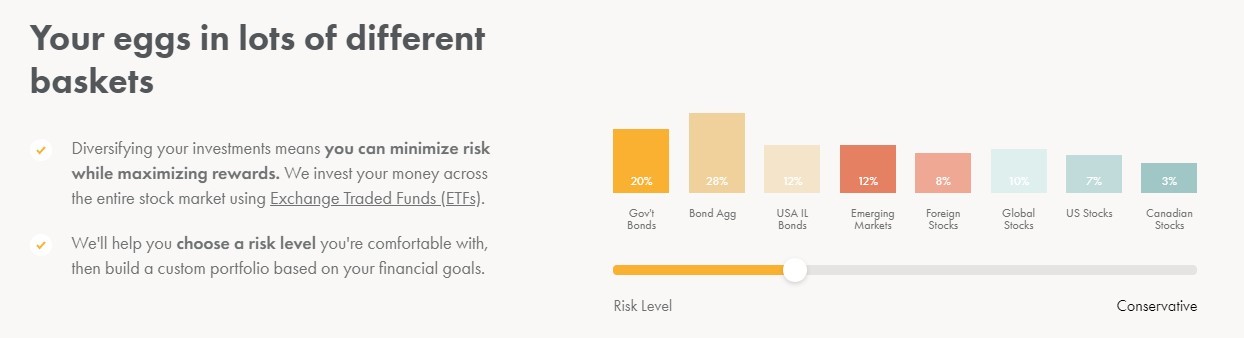

When you sign up for Wealthsimple you are asked a series of questions which determine your comfort with risk. They keep costs down by having 3 different bundles of ETF’s and bonds. Below is a their sample investment mix for someone with moderate risk tolerance. If you were a retiree you would have a much lower risk tolerance.

From what I have seen, the three bundles are:

From what I have seen, the three bundles are:

- 33% ETF’s and 67% bonds – People with a very low risk tolerance like retirees or people saving to pay for something (car, tuition…)

- 67% ETF’s and 33% bonds – Most people with a moderate risk tolerance

- 80% ETF’s and 20% bonds – People with a a higher risk tolerance and long investment horizon (i.e. 40 year old saving for retirement at 70 years old)

What Is The REAL Cost of Wealthsimple Fees?

Wealthsimple charges most people .5% for all of this management and diversification. You also need to add in the ETF fees and here again Wealthsimple is working for you. Because they are buying millions of dollars in ETF’s they have negotiated their ETF fees down to an average of .2% (Yes, that is 30% less than you can buy ETF’s as an individual).

That makes your whole Wealthsimple fee about .7% (.5% + .2%). Compare that to what most people have invested in for the last 50 years, Mutual Funds, which charge an average of 2.25% and you can see that Wealthsimple is about 66% cheaper.

If you invest more than $100,000 will them their fee drops to .4% making your total cost about .6% which is 75% less expensive than mutual funds.

If you invest more than $100,000 will them their fee drops to .4% making your total cost about .6% which is 75% less expensive than mutual funds.

If all those numbers are just too confusing think of it this way. A recent Canadian study showed that Mutual funds cost the average person $323,000 over their lifetime. Wow that is alot of cash paid to your investment advisor or bank or … . If you had just bought ETF’s using Wealthsimple or other roboadvisor your cost would have been closer to $70,000 over your lifetime. I don’t know about you that the difference of a quarter of a million dollars is something I want to keep in my pockets.

How To Get A Discount On Wealthsimple Fees

If you open an account with Wealthsimple they will not charge any fees on the first $5000 for the first year. However, you can double that to $10,000 without fees if you use a reference code from a current Wealthsimple customer… like me. I also get $10,000 invested without fees for making the reference, so I would certainly appreciate it if you would click my referral code HERE.

Note that I am NOT affiliated with Wealthsimple and they are NOT paying me in ANY way for this or any other article.

Are there Special Investment Choices?

If you want Wealthsimple to be more specific than the general market, they offer to limit your investments to so called “ethical funds” or “Halal funds“. Most people will not want these are they, by definition, restrict your options.

You can also put your money into a TFSA or RRSP or a general taxable account. You decide what is right for you.

0 Comments